LLC stands for "Limited Liability Company", or limited liability company. LLCs are increasingly popular business structures today and knowing how they work is key for any entrepreneur or person interested in business.

If you have questions about what an LLC is, how they work or what it can provide to an entrepreneur, you are in the right place. In this complete guide, you will be able to clear up all the doubts you have about LLCs in the United States.

Let's start with the first thing!

What is an LLC?

A limited liability company, or LLC, is a US legal entity used to own, operate, and protect a business. By having an LLC, business owners are protected from personal liability for their company's debts or liabilities. Instead, the liability falls on the LLC, meaning the company is considered its own legal entity. In the event of bankruptcy or a legal dispute with the company, LLCs protect the owners' personal assets, such as bank accounts, homes, and cars. Thanks to these advantages of LLCs, they are very popular among small and medium-sized businesses.

What are the advantages of a US LLC?

Registering an LLC in the United States is extremely popular among freelancers and small or medium-sized businesses, both in the United States and in the rest of the world. This is due to the numerous benefits of LLCs compared to other existing business structures.

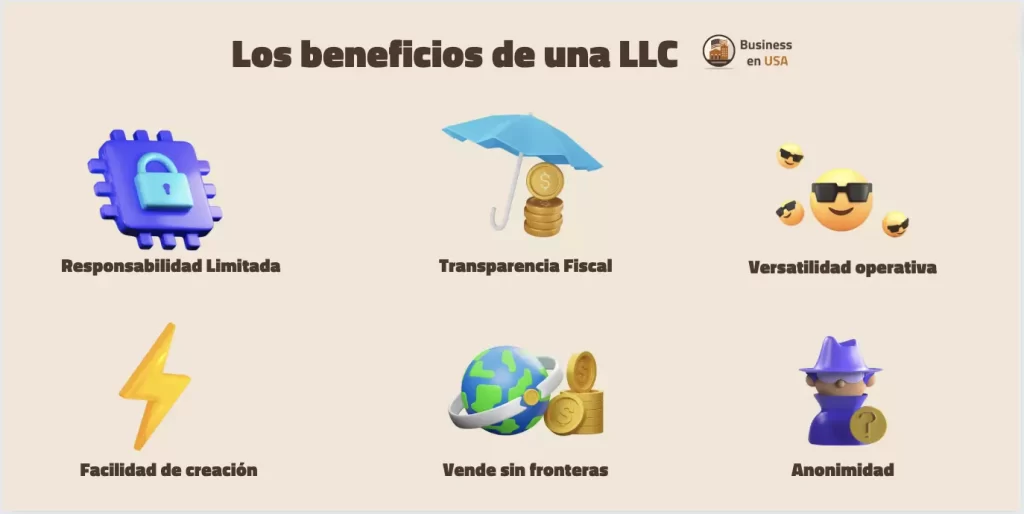

Fiscal Transparency

Tax responsibility passes to the personal tax return of the owners of the LLC, which is known as "Pass Through Taxation" or tax transparency.

In this way, foreign non-resident LLCs do not pay taxes in the United States.

Limited liability

The main advantage of an LLC is in its name: the limited liability of its members.

The owners' personal assets can be protected from the company's debts and lawsuits against the company when an owner uses an LLC to do business.

Ease of creation and management

Creating an LLC is very simple, and can be done in a matter of days. It can be done online, and the cost of creating an llc is cheap.

Also, operating an LLC is very simple. It has very few formal requirements and a lot of flexibility to operate according to how each company likes within the legal framework.

LLCs can have as many members as the leaders agree, the members can freely determine how they distribute profits (by shares, by results, by contributions...) and can draft an operating agreement (Operating Agreement) to introduce any change in its operation.

Operate in the United States and the world

With an LLC, you can open the door to international business. You can have a bank account in the United States, and have the credibility and legal framework you need to operate in the United States as with any part of the world.

Anonymity

There are certain states in the USA where LLCs are completely anonymous. Member names are not requested or published in any public record. This is of great interest to entrepreneurs who want to keep a low profile and not associate the success of their business with themselves.

What are its disadvantages?

The cost of LLCs in certain states can be considered a disadvantage. LLCs are formed and registered at the state level, so the process of creation, maintenance and their associated costs may vary between states. LLCs in New Mexico cost $50 usd, for example, while in Massachusetts $500, or LLC of Delaware that have a "Franchise Tax" of $300 annually.

Another disadvantage is that in an LLC, it is not as easy to transfer from one party to another as shares of a corporation. Except as provided in the operating agreement, some states require that an LLC be dissolved whenever there is a change in ownership. This does not make them ideal societies for obtaining external investment, for example.

How does an LLC work in the United States?

Now that you know what an LLC is and what its advantages or disadvantages are, let's go into detail about how it works.

Your registration

An LLC can be opened by any person over 18 years of age, resident in the United States or a foreigner. LLCs can be single member (LLC unipersonales) or multi-member (corporations).

The members

The owners of an LLC have shares in the company, which are defined at the time of registration of the LLC.

The operating agreement

Once the LLC is registered, members are advised to draft and sign an operating agreement, where they will define how the company will operate:

- The roles

- How the dividend distribution will be

- How ownership is transferred

- The dissolution of the LLC

- How the search for capital will work

- etc....

This agreement gives members flexibility to manage your LLC. If not drafted, the LLC will be governed by the state's standard rules.

LLC Management

The management of the LLC can be carried out as follows:

- All members manage it

- A hired manager (non-member) manages it

- A management committee (made up of members) manages it

Members can act as passive investors in the company, in which case their only participation in the company is financial.

Voting system

The owners of an LLC have voting rights based on the ownership they hold in the LLC. For example, if one member has 25% of the LLC, but another has 50%, the vote of the member with 50% of the shares will count twice as much as that of the member with 25%.

If voting rights have not been otherwise set forth in the operating agreement, the LLC must follow the voting rules established by the state in which the LLC is incorporated.

Taxation

LLCs have the option to choose the way in which they are taxed.

- Multi-member LLCs work with Pass-Through Taxation, meaning that the LLC does not pay taxes as a company, but instead each member declares taxes on their personal tax return on their percentage of shares.

- If your business is a sole proprietor LLC, the LLC itself does not have to file a return with the IRS. However, as a sole proprietor, you must report all profits and losses when filing your personal taxes in your country of residence.

- Single-member and multi-member LLCs can also choose to file taxes as a corporation, which can reduce the amount your LLC owes (especially for LLCs that operate in the USA). This is usually done to access certain tax exemptions and deductions.

Steps to follow to register an LLC

If you are convinced that registering an LLC is a good option for you, discover our complete guide on how to create an LLC in the United States. Here we will quickly detail the steps to follow:

- Choose the state where you want to register your LLC:There are 50 states where you can register an LLC, and each has its advantages and disadvantages.

- Define the members of your LLC: Who will be the owners of the LLC and what will be their participation in the company?

- Choose the name of your LLC: Your LLC name must be unique in the state and contain the term LLC or Limited Liability Company. There are certain terms prohibited by the State.

- Designate a registered agent: A registered agent will be a person over 18 years of age who is a resident of the state where you register your LLC. She will be in charge of transmitting official documents to members. There are several companies that offer registered agent services.

- Complete and submit the "Articles of Organization": This document downloadable on each state's website is necessary to form your LLC. Here you will find all the key information about your business. It has a cost depending on each state.

- Write the Operating Agreement: It is the contract that specifies the operation of the LLC. It is not mandatory.

- Request the EIN: The EIN or Employee Identification Number is necessary to open a business bank account, hire employees, etc...

- Open a business bank account: A business bank account is key to separating your personal assets from those of the company. It will also make accounting much easier.

- Meet annual obligations: Depending on each state, you will have different obligations (annual reports, taxes, IRS statements). Failure to comply with obligations may lead to fines or closure of the LLC.

How does an LLC compare to other business structures?

The most common alternatives to the LLC are "corporations", "partnerships" and "sole proprietorships". Let's compare them with LLCs!

LLC vs. Corporations

A corporation is more formal, involving bureaucracy, continuous paperwork and stricter reporting than what a Limited Liability Company usually requires. Instead of partners, there are shareholders. In this way, shares can be issued to raise funds. Additionally, it is necessary to proceed with the election of a board of directors to direct the operations of the corporation. Also, it is important to clarify that LLCs can choose to be taxed as corporations, but without changing their legal status as an LLC.

LLC vs. Partnerships

Partnerships or companies include two or more owners who agree to share the assets, liabilities and legal burdens of a jointly owned company. Regarding LLCs, partnership-type companies do not have limited liability nor are they considered legal entities in themselves.

LLC vs Sole proprietorships

With a sole proprietorships or self-business, there is a single owner who has full control of the company. Sole Proprietorships can benefit from tax transparency. Their biggest drawback is that they do not protect the liability of the owner, who remains solely responsible for all the company's debts.

Frequently Asked Questions

Is it easy to open an LLC in the United States?

Registering an LLC is a very easy process that can be done online, and takes about 2 to 3 weeks. The costs of an LLC will vary by state, but at the business level, they do not represent too high costs. Opening an LLC in the United States is then easy, accessible and fast for anyone in the world.

How much does it cost to open an LLC?

The cost of opening an LLC will depend on the state in which you want to register it. States like New Mexico have a cost of $50, without annual taxes. Delaware, for example, has a registration fee of $90 and $300 annually.

As you can see, the conditions vary greatly depending on each state, so it is important that you inform yourself in depth about the costs and requirements of the state in which you want to open your LLC.

In what state should I open my LLC?

The most common states for nonresidents to establish limited liability companies are Delaware, Wyoming, and New Mexico. It is recommended to be careful because the fact that they are widely used does not automatically make them the most convenient option for you.

If you are a resident of the United States, our usual recommendation is that you incorporate the limited liability company in the state in which you live.

Here you can study this question in detail: How to choose the state for my LLC?

What types of businesses typically benefit from opening a US LLC?

The companies that benefit most from the establishment of American LLCs are those dedicated to e-commerce, dropshipping, international freelancers, and other forms of Internet business. For digital companies with activities abroad, LLCs are usually quite useful.

How many members can an LLC have?

The number of members that an LLC can have is not limited in any way, neither by a minimum nor a maximum. If you wish, you can form a limited liability company (LLC) with a single member and be the sole owner of it, or you can form an LLC with dozens of members.

What is a Non-Resident LLC?

A non-resident LLC is an LLC whose owners do not reside for tax purposes in the United States. Even though you are not a resident of the USA, with an American LLC you will be able to benefit from better tax conditions than the business structures in your country, open new business opportunities with the USA or the world, access to do business with platforms such as Amazon or Stripe, etc...

What are the different types of LLC in the USA?

In the United States, there are different types of LLC:

- One-person LLC: The one-person LLC is managed by a single person.

- Multi-member LLC: Managed by several partners. Each partner then has a percentage of shares in the LLC, and depending on that, voting rights.

- L3C: An L3C is a type of for-profit LLC whose primary motive is charitable or educational.

- Series LLC: Is a form of LLC in which the bylaws specifically permit the unlimited segregation of member interests, assets and operations into independent series.

- PLLC: A professional limited liability company is designed for licensed professionals, such as lawyers, doctors, architects, engineers, accountants and chiropractors.

- Restricted LLC: This type of US LLC is not taxed for the first 10 years of its incorporation. However, they also cannot make distributions to members. This must appear in the Article of Organization.

Written by

Ignacio Navarro

Ignacio Navarro is a Certified Public Accountant, graduated in 2020 from the National University of Tucumán. Founder of Start Companies since 2023, he advises clients worldwide on forming LLCs in the United States and on proper tax filing. His expertise combines legal, tax, and practical knowledge, offering a comprehensive service that spans from company formation to bank account setup and sales platform integration.