Corporations are extremely useful tools in creating businesses anywhere in the world. This is because having a corporation as the legal structure for your businesses allows you to obtain numerous benefits, from legal to tax, in addition to better financing.

For this reason, today we bring you a complete guide to corporations in the United States and how to create them. By following this guide, you will be able to understand what a corporation is, what its advantages are and what you should take into account to know what type of corporation to create according to the nature of your business. Let's get started!

What is a corporation?

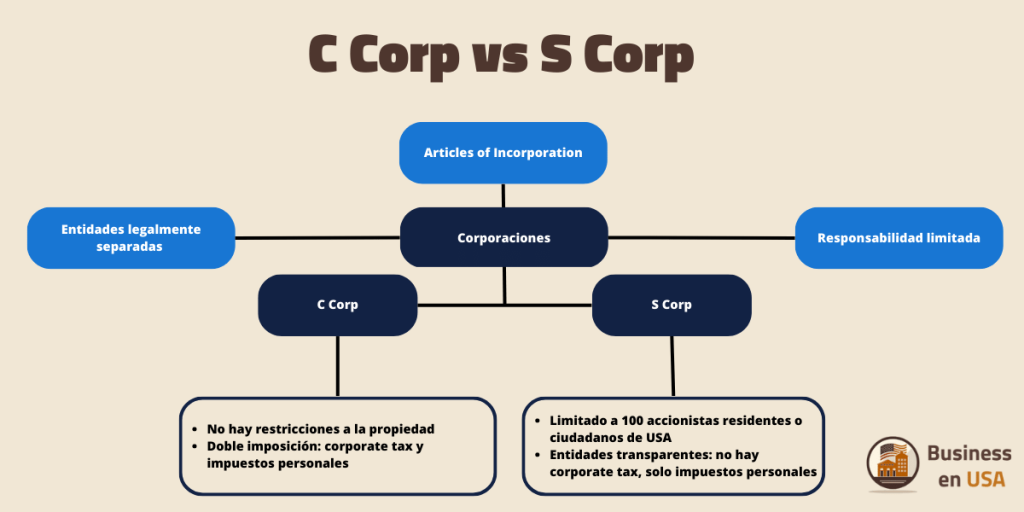

A corporation is a business entity separate from its owners and shareholders. In the United States, a corporation is a legal person, so it has the same rights as an individual: own property, sell it, sue, be sued, sign contracts and even create new corporations.

A corporation is owned by its shareholders, who elect a board of directors to oversee the activities of the organization. Corporations are then governed by their corporate bylaws and board of directors, and these further govern the admission or removal of new companies, new shareholders, as well as the distribution of the company's shares and much more.

Finally, corporations can be for-profit or non-profit, so they serve as both businesses and charities. Let's dive into this!

The different types of corporations

There are several types of corporations, and it is necessary to be very clear about the difference between each of them in order to understand which one is the most convenient for your business. That is, each of them has a different scale and approaches when it comes to managing a business, both for profit and non-profit organizations.

In the United States there are at least 3 types: C-Corporations and S-Corporations, but we also have No-Profits-Corporations.

The S-Corps

S-Corporations, or S corporations, are business entities that offer limited liability, "pass-through taxation", and are limited to 100 shareholders who must be American citizens or residents. Due to these characteristics, they are popular for small and medium-sized businesses in the USA.

Like LLCs, S-Corp are transparent entities, or pass-through: They transfer income, losses, deductions or credits directly to shareholders, without paying any federal tax. Shareholders report this activity on their personal tax returns, which allows S corporations to avoid double taxation on business income.

The biggest disadvantage of S-Corps is that they are often subject to scrutiny by authorities for being linked to some irregularities in tax collection in the past.

C-Corps

C corporations in the United States are very similar to S corporations:

They are for-profit, incorporated and governed by the same state corporation laws, offer limited liability, and observe the same internal formalities (board of directors, corporate bylaws, shareholder meetings, ...).

The main differences with S-Corps are:

- C corporations have no ownership restrictions: they have no limits or conditions for shareholders, and they can issue different types of shares.

- The way they are taxed: The profits of a C-corp are taxed on the corporation when earned and on shareholders when distributed as dividends, which creates double taxation.

Non-profit corporations

The structures of non-profit corporations are, in reality, quite similar to for-profit corporations, however, those who finance them are not shareholders, but donors, and like the former, they have the possibility of modifying the decisions made by the corporation.

These, however, non-profit corporations do not generate profits, since they are dedicated to some type of public service or some “altruistic” mission. Donations can come from a wide range of sources, including other corporations, and are excellent tax deductibles for them.

What are the advantages of corporations?

Clearly, there are many advantages that invite you to create a corporation. It is not for nothing that they are the most used business structure in the world.

Limited liability

The first advantage has already been mentioned above, and that is that corporations offer limited liability protection to their shareholders. They are not personally responsible for the debts and obligations of the company, so creditors cannot claim the personal assets of the owners to pay the company's debts.

Ease of transfer of ownership

Ownership of a corporation is usually easily transferable through the issuance or sale of its shares (although S-Corps have certain limitations, as we saw above). Shares are bought and sold very easily on the stock market. This also allows them to be able to raise funds easily, a luxury that most other business entities do not have.

For this same reason, corporations are often the preferred structure for entities that provide financing (banks, VCs, Business Angels...).

Corporate credibility

Having a well-known and highly reputable business structure, such as corporations in the United States, will provide credibility to your business. Potential investors, lenders, suppliers, clients and employees will know that your business is serious and is projected for the long term.

Tax advantages

Depending on how you have chosen to pay taxes (S-Corp or C-Corp), the tax advantages will be different.

Although C corporations are subject to double taxation, S corporations are fiscally transparent entities that have tax advantages, depending on how their income is distributed.

S corporations have the luxury of dividing their income between the company and shareholders, allowing for some tax flexibility. Any income designated as the owner's salary will be subject to self-employment tax, while the rest of the company's dividends will be taxed on the personal tax return.

Perpetual existence

Corporations are technically immortal: if they are not dissolved by their board of directors, or liquidated by the State, corporations can live forever, even after the death of all their investors. Technically, as long as there is money flow and income exceeds expenses, a corporation will continue to be alive.

What are the disadvantages of corporations?

Just as there are advantages, there are also a series of disadvantages that must be taken into account before creating a corporation. Primarily, these are related to regulations and the added responsibilities of being the owner or co-owner of an organization.

A creation process and tedious formalities

Opening and maintaining a corporation is not as simple as opening an LLC. Filing the articles of incorporation with the Secretary of State may be quick, but then, there is extensive paperwork to properly determine and document the details of the organization and its ownership, as well as to maintain it. For example, it is necessary to write and maintain the corporation's bylaws, appoint a board of directors, create a change of ownership agreement for shareholders, issue stock certificates, have annual meetings and record them, make regular reports, … We will look at this in more detail below.

Double tax burden

As we have already explained before, C corporations have a double tax burden: they first have a tax on corporate profits and then shareholders must pay personal taxes when they receive dividends.

How to open a corporation in the United States?

In the United States, a corporation can be created in 9 steps, these are well described in the country's own laws and, although depending on the State, these steps may vary a little, generally throughout the country it is the same process. Below we will describe the steps:

1. Choose a name for your corporation

Choosing the name of your corporation is the first step for your business. It is not only important to consider the aspects of marketing and brand credibility, but also respect certain legal requirements:

- You must add an entity identifier, that is, after the trade name, you must add the acronym Inc, Co, Ltd, etc. which stand for Incorporated, Company and Limited.

- You may not use names of public agencies or government entities, or words like Bank, Trust, Trustee or Credit Union.

2. Appoint directors

For US regulators, it is necessary that, when creating a corporation, the directors of the company are immediately appointed. The directors are responsible for managing the corporation and electing the company's directors.

It is important to note that owners can appoint themselves as directors or other people, and that this board of directors can change later.

3. File the Articles of Incorporation

To create a new corporation, you must file the Articles of Incorporation with the Secretary of State where you decide to register your corporation. Typically, this can be done 100% online on the website of the state in question.

In this legal document, all the details of the company will be established: its name, the main place of business, the purpose, the address of the registered agent and the names and addresses of the incorporators, as well as the initial board of directors.

4. Write the bylaws of the corporation

The bylaws of a corporation are the rules and regulations that regulate its operation. These bylaws usually include:

- The functions assigned to each officer

- How business decisions will be made

- Where and when annual shareholder meetings will be held

- How and when shares will be issued

- The percentage of shareholders necessary to make decisions

- Where and when dividends are paid

5. Hold the first meeting of the Board of Directors

Once the corporation is established and the bylaws drawn up, it is necessary to carry out the first formality: a first one for directors. In this meeting, it is common to cover:

- The adoption of the corporation's bylaws

- The official appointment of the corporation's officers

- Obtaining authorization to issue shares

- The choice of being taxed as a C-Corp or S-Corp

6. Share issue

A corporation is owned by its shareholders, who make a capital contribution in exchange for shares. A share then represents a unit of ownership of the corporation.

It is necessary for your corporation to execute the share certificates and update the corporation's share book, where it will keep track of who owns shares and how many they own. Corporations are required to keep track of how many shares they issued, who owns them, and how many are outstanding.

7. Write a Shareholder's Agreement

The Shareholder's Agreement is an agreement between shareholders where the operation of the issuance and transfer of shares is agreed. Its objective is to guarantee that shareholders receive fair treatment and that their rights are protected. It is optional, but it is quite advisable to have one to avoid any type of disagreement in the future.

For example, this agreement determines how the property will be managed if a shareholder dies, retires, becomes incapacitated or leaves the company, for example. It also allows shareholders to make decisions about which external parties can become future shareholders and provides guarantees for minority positions.

8. Obtain a company identification number

The EIN is a unique identifier that is assigned to a company so that it can be easily identified by the Internal Revenue Service (IRS). It is also necessary to open a company bank account, hire employees and much more. You can obtain an EIN quickly and free on the website from the IRS.

9. Obtain permits, licenses and DBA for companies

Most businesses need some type of business license or permit to operate, but the requirements will depend on the state where you have registered your corporation and your industry. The weapons, tobacco or alcohol industries, for example, often require additional licenses to operate. You can check your state's specific requirements here.

Also, if you plan to do business under a name other than the corporation's official name, you will also need to register a DBA.

What if I need to dissolve my corporation in the future?

To dissolve a corporation there are also a series of steps that you must follow, and that finally liquidates the company, leaving everything in order and compensating those affected by its end. These are the major steps to follow:

- Convene a board meeting to formally propose the dissolution of the corporation. A vote must be held and the minutes of the meeting must be recorded and preserved.

- File a certificate of dissolution with the Secretary of State. Documentation can be submitted online.

- Notify the IRS of your intent to dissolve the business. Pay all taxes owed to both the state and federal government in order to obtain a “dissolution consent” or “tax liquidation.”

- Close everything else: Close all bank accounts, lines of credit, and utility accounts you have in your name. corporation or company. Notify all your customers, suppliers and employees of the dissolution of your corporation. Close your EIN

- Keep records of everything, to prove that you have closed and left everything in order, in case it becomes necessary.

Conclusion

The business world in the United States is quite dynamic, and one of the best ways to enter it today, especially if you want to grow your business, is with a corporation. Although they are legal entities with many formalities, they are the best solution when you are looking to have a large business that distributes ownership through the issuance of shares.

Written by

Ignacio Navarro

Ignacio Navarro is a Certified Public Accountant, graduated in 2020 from the National University of Tucumán. Founder of Start Companies since 2023, he advises clients worldwide on forming LLCs in the United States and on proper tax filing. His expertise combines legal, tax, and practical knowledge, offering a comprehensive service that spans from company formation to bank account setup and sales platform integration.