Definition of C-Corp and S-Corp

Both C-Corps and S-Corps are corporations. Before going into detail about each one, let's understand what a corporation is.What is a corporation

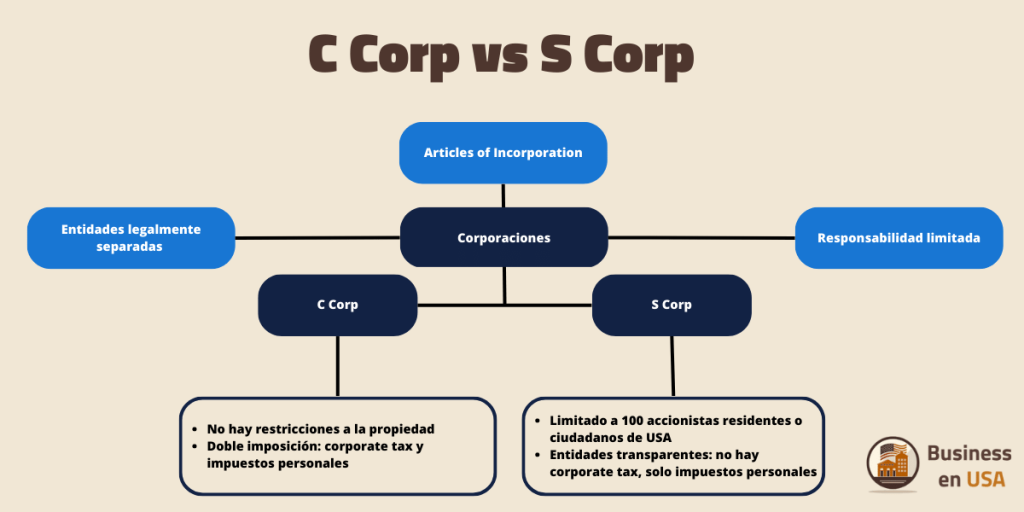

A corporation is an American business entity that is created by filing articles of incorporation with a secretary of state. The owners of a corporation are shareholders and elect a board of directors to make decisions on behalf of the company. Additionally, a corporation can issue stock to raise capital and, in some cases, can go public. Also, corporations offer limited liability: shareholders are not personally liable for the corporation's debts. However, unlike other business structures, corporations must comply with legal requirements and corporate formalities for their proper functioning.What is a C-Corp

C-Corp status isthe tax structure that the IRS applies by default for a corporation. The main characteristic of the C-Corp is that they are subject to double taxation: first they pay corporate taxes, and then shareholders must pay personal taxes on profits from dividends or sale of shares. The main reason for being taxed as a C-corp is that, unlike S-Corps, there are no restrictions on who can own shares, nor are there limits on the total number of shareholders.What is an S-Corp

The S-Corp tax status is not subject to double taxation. The IRS considers them to be pass-through entities, so they do not pay corporate taxes and taxes will only be collected from the income of their shareholders. However, to qualify as an S-Corp, the IRS indicates that :- You cannot have more than 100 shareholders

- Only one class of shares must be issued

- Ownership is limited only to American individuals, some trusts, and non-profit organizations.

- Not be an ineligible corporation

- Be a domestic corporation

C-Corp vs S-Corp: Comparison

Now that we have defined both tax structures, let's put them face to face and compare them to help you more easily decide which one suits your business.| Features | C-Corp | S-Corp |

|---|---|---|

| Training | Articles of Incorporation (C-corp is the default tax structure for corporations) | Articles of Incorporation + IRS Form 2553. |

| Taxes | Double taxation: corporate income and personal income | Only a tax on personal income |

| Loss deduction | They cannot be deducted on personal tax returns | Can be deducted on personal tax returns |

| Filing taxes | Every 3 months | 1 time per year |

| Number of Shareholders | Ilimitado | Maximum of 100 |

| Type of Shareholders | All eligible entities | Individuals and certain estates, trusts, tax-exempt organizations |

| Origin of Shareholders | No restrictions | American citizens or permanent residents |

| Share Classes | No restrictions | Only one class of shares can be issued |

| IRS scrutiny | Normal | Above average in the balance of salary vs. dividends |

| Capital Financing | Easier to raise capital | More difficult to raise capital |

Similarities between C-Corp and S-Corp

If we compare both structures we will find several similarities between them.Personal liability protection

State laws establish that corporations are legal entities separate from their owners. This means that shareholders are not personally liable for the company's debts, and their personal assets are protected from potential creditor claims.Structure

In both types of corporations, shareholders elect directors to oversee the daily operations of the business. As the corporation generates profits, dividends are distributed to shareholders based on the number of shares they own.Legal obligations

To maintain compliance, both C-Corps and S-Corps must:- Issue shares

- Adopt statutes

- Hold annual meetings of directors and shareholders

- Keep meeting minutes

- Emitir resoluciones corporativas escritas para decisiones importantes

- Submit annual reports to the state government

- Pay annual fees

Differences between C-Corp and S-Corp

Training

By submitting the Articles of Incorporation to the secretary of state, corporations begin their existence as C corporations. You can become an S corporation by filing IRS Form 2553. To obtain S corp status in a given year, you must file Form 2553 by March 15 if operating in a calendar year. Those corporations that operate in a different fiscal year can submit it before the 15th day of the third month of the fiscal year.Imposition

The main reason to choose S corp status is to save on taxes. As we mentioned, C-Corps have double taxation: they must pay corporate taxes on their profits and then the shareholders pay taxes again on what they receive in the form of dividends. Choosing S corp status allows you to avoid double taxation. C corporations file taxes using Form 1120, while S corporations file Form 1120-S.Property

The main advantage of C-Corp is that it offers greater flexibility in the sale of shares. Unlike S-Corps, C-Corps have no limits on the number of shareholders, their nationality or citizenship, or the types of shares they can issue. This facilitates its growth and its possibility of raising investments.Deductions from profits to shareholders

C-Corps can deduct business benefits provided to shareholders who are also employees (life insurance, disability, etc...). These are not taxable to the shareholder, as long as the benefits extend to at least 70% of the employees. By contrast, an S corporation cannot do so, and these profits become taxable to a shareholder who owns more than 2% of the shares.

Does C-Corp or S-Corp status suit me?

There is no generic answer to this question, and it will depend on the situation of each entrepreneur and their company.In what situations may it be preferable to choose a C-Corp?

Entrepreneurs typically choose to open a C-Corp when the following conditions are met:- C-Corp taxation would result in lower taxes than taxing as an S-Corp.

- No large dividend distributions will be made to shareholders, which reduces the problem of double taxation.

- It plans to go to IPO, and raise investment easily, without any type of restriction on who can invest in the company.

- You want the shares to be freely and easily transferable.

- You want to issue different types of shares.

In what situations may it be preferable to choose an S-Corp?

Opening an S-Corp is usually preferred when:- You have no plans to take your company public, you do not seek to have more than 100 shareholders or have types of investors that are not permitted by Subchapter S.

- The corporation will distribute its income to shareholders.

- You have no plans to issue preferred shares. Having a single type of actions for all members is not a problem.

- Shareholders' tax liability, taking into account their personal income tax rate, deductions and exemptions, will be lower using a pass-through entity compared to a separate tax entity.

Conclusion

Making the decision between opening an S-Corp or a C-Corp is not obvious. Especially when it is very difficult to know what situation your company will be in in 10 or 20 years... Additionally, tax issues can vary greatly depending on one's situation. Therefore, at Business in USA, we always recommend having our legal and financial advice before making any type of decision. Finally, it is important to note that if you decide on the S-Corp tax structure, it is possible to go back. You only need to file a written statement with the IRS, along with a consent signed by the majority of your corporation's shareholders. Get professional help to open your Corp- Business experts in the USA

- Legal and accounting team

- Free first consultation

Written by

Ignacio Navarro

Ignacio Navarro is a Certified Public Accountant, graduated in 2020 from the National University of Tucumán. Founder of Start Companies since 2023, he advises clients worldwide on forming LLCs in the United States and on proper tax filing. His expertise combines legal, tax, and practical knowledge, offering a comprehensive service that spans from company formation to bank account setup and sales platform integration.